by Joanne Danganan, Jeepney Hub Content Development Director

Click Image for Source

Click Image for Source I have compiled 5 of the most important milestones for a sound and happy wallet. Keeping in mind that not everyone’s road to financial independence is the same, and not everyone’s story follow the same plot or timeline, I did not limit these milestones to any age range. Of course, the sooner you start, the sooner you can take your finances by the lapel and have it work for you. After all, one of the main ingredients to success is making sound financial decisions. Let’s get started!

1. Maintain a short-term emergency fund and start a long-term emergency fund.

Since emergencies typically come at the worst of times (which is anytime), having an emergency fund (EF) before you start tackling credit card debt, investing, or doing anything else with your money is pretty wise. You won’t want to sacrifice paying down your debt or setting aside a large windfall for your investment portfolio in case you have to pay for an unexpected and/or huge medical bill – by having that EF around, you won’t have to choose which one to pay!

A short-term EF can be used to pay for unexpected car repairs (or towing fees on top of a parking violation, like I experienced just last month), unexpected health expenses (wisdom teeth extraction, anyone?), and house appliance repairs (for those who own appliances). Having a short-term EF ensures that you won’t be set back a couple hundred bucks in a particular month or two. It will also help you avoid charging it on your credit card, which can be way more expensive in the long run if that charge isn’t paid back immediately.

To maximize the use of an emergency fund, start one for the long term by saving between 3 and 6 months worth of living expenses – rent, bills, and sustenance. This will cushion your fall if you experience any period of unemployment from a sudden layoff, for example.

A great blog called Money Crashers has a great, in-depth article about emergency funds. I personally use online savings accounts to house my emergency funds (Capital One 360, Ally Bank) for their relatively high yields.

2. Pay off high-interest credit card debt.

If not used wisely, high-interest credit cards can get you into real trouble. If you are swiping that piece of plastic often enough, but are unable to pay off the balance at the end of each month, you are potentially throwing away hundreds or even thousands of dollars in interest each year.

Back in college, I had a bad habit of just paying the minimum every month. I thought, “WOW, this is great! I can borrow hundreds of dollars for just $15 a month?!” Oh, how naive of me...

By the time I maxed out my first credit card, I was paying 26% in interest on top of my $700 principle. In total, I easily wasted at least $500 in interest by only paying just a little over the minimum payment, thanks to my high interest rate. And since I kept swiping that piece of plastic, my balance just flatlined – I wasn’t making a single dent!

When I finally realized I could be saving all that cash, I decided to do something drastic. I put a portion of one of my tax refunds towards paying off my credit card debt and voila – my life changed overnight. My credit score improved by 100 points (I’m not exaggerating), and I had the wonderful opportunity to put aside more money in savings since I no longer had pesky monthly payments to worry about.

The point is, credit card debt is expensive. If you want to start becoming (or stay) financially sound, stop using that piece of plastic dangerously and start using it wisely. David at Money Under 30 goes into great detail about how you can do just that.

3. Set aside money for retirement.

Don’t put off for tomorrow what you can do today. That includes setting money aside for your retirement – our good friend Compound Interest begs you to start today.

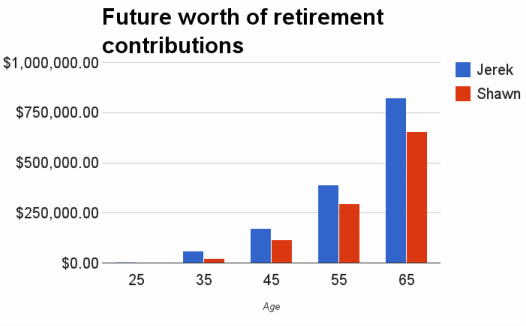

To illustrate, let’s follow two 25-year-old brothers: Jerek and Shawn. Jerek graduated with his BA and landed a job at a non-profit. He immediately signed on to set aside $300/month (or $3,600 annually) toward a retirement plan. Shawn also graduated with his BA and went straight to medical school. Seven years later, he was able to set aside $400 a month (or $4,800 annually) after starting as a doctor at a local hospital.

Assuming Jerek and Shawn both set aside consistent amounts and assuming they retire at the same age of 65, let’s see how the numbers compare:

Since Jerek started saving at age 25, he already has a huge leg up. Assuming a 7% return, his $3,600 annual retirement contribution would be worth $822,903 at age 65. On the other hand, Shawn couldn’t put aside any serious money until he became a doctor at age 32. Therefore at 65, also assuming a 7% return, his $4,800 annual retirement contribution would be worth $655,603. That’s a difference of $167,300!

1. Maintain a short-term emergency fund and start a long-term emergency fund.

Since emergencies typically come at the worst of times (which is anytime), having an emergency fund (EF) before you start tackling credit card debt, investing, or doing anything else with your money is pretty wise. You won’t want to sacrifice paying down your debt or setting aside a large windfall for your investment portfolio in case you have to pay for an unexpected and/or huge medical bill – by having that EF around, you won’t have to choose which one to pay!

A short-term EF can be used to pay for unexpected car repairs (or towing fees on top of a parking violation, like I experienced just last month), unexpected health expenses (wisdom teeth extraction, anyone?), and house appliance repairs (for those who own appliances). Having a short-term EF ensures that you won’t be set back a couple hundred bucks in a particular month or two. It will also help you avoid charging it on your credit card, which can be way more expensive in the long run if that charge isn’t paid back immediately.

To maximize the use of an emergency fund, start one for the long term by saving between 3 and 6 months worth of living expenses – rent, bills, and sustenance. This will cushion your fall if you experience any period of unemployment from a sudden layoff, for example.

A great blog called Money Crashers has a great, in-depth article about emergency funds. I personally use online savings accounts to house my emergency funds (Capital One 360, Ally Bank) for their relatively high yields.

2. Pay off high-interest credit card debt.

If not used wisely, high-interest credit cards can get you into real trouble. If you are swiping that piece of plastic often enough, but are unable to pay off the balance at the end of each month, you are potentially throwing away hundreds or even thousands of dollars in interest each year.

Back in college, I had a bad habit of just paying the minimum every month. I thought, “WOW, this is great! I can borrow hundreds of dollars for just $15 a month?!” Oh, how naive of me...

By the time I maxed out my first credit card, I was paying 26% in interest on top of my $700 principle. In total, I easily wasted at least $500 in interest by only paying just a little over the minimum payment, thanks to my high interest rate. And since I kept swiping that piece of plastic, my balance just flatlined – I wasn’t making a single dent!

When I finally realized I could be saving all that cash, I decided to do something drastic. I put a portion of one of my tax refunds towards paying off my credit card debt and voila – my life changed overnight. My credit score improved by 100 points (I’m not exaggerating), and I had the wonderful opportunity to put aside more money in savings since I no longer had pesky monthly payments to worry about.

The point is, credit card debt is expensive. If you want to start becoming (or stay) financially sound, stop using that piece of plastic dangerously and start using it wisely. David at Money Under 30 goes into great detail about how you can do just that.

3. Set aside money for retirement.

Don’t put off for tomorrow what you can do today. That includes setting money aside for your retirement – our good friend Compound Interest begs you to start today.

To illustrate, let’s follow two 25-year-old brothers: Jerek and Shawn. Jerek graduated with his BA and landed a job at a non-profit. He immediately signed on to set aside $300/month (or $3,600 annually) toward a retirement plan. Shawn also graduated with his BA and went straight to medical school. Seven years later, he was able to set aside $400 a month (or $4,800 annually) after starting as a doctor at a local hospital.

Assuming Jerek and Shawn both set aside consistent amounts and assuming they retire at the same age of 65, let’s see how the numbers compare:

Since Jerek started saving at age 25, he already has a huge leg up. Assuming a 7% return, his $3,600 annual retirement contribution would be worth $822,903 at age 65. On the other hand, Shawn couldn’t put aside any serious money until he became a doctor at age 32. Therefore at 65, also assuming a 7% return, his $4,800 annual retirement contribution would be worth $655,603. That’s a difference of $167,300!

Though Shawn eventually contributed slightly more per year than Jerek, Jerek still earned a little over $150,000 dollars more overall. This is because Shawn had to defer earning income in exchange for his MD and simultaneously had to defer contributing to retirement for seven whole years, putting Jerek at a huge advantage from the start.

The lesson here is all about the incredible principle of compound interest. The earlier you save, the larger your return will be. At a decent return, even 7 years makes a huge difference. So again, don’t put off for tomorrow what you can do today. Even $50 a month now can mean thousands of dollars down the line.

Personally, retirement benefits are the first thing I look for in a potential employer. Many employers match a percentage of your retirement contribution - which I consider FREE money! If your employer offers this, you should have been taking advantage of this yesterday.

If you don’t have that privilege, consider opening an individual retirement account (IRA) on your own (see number 5). Personally, I have a rollover IRA Fidelity from my first job out of college, but lately I’ve been eyeing Vanguard’s IRAs - a friend of mine loves investing with Vanguard so I will personally be looking into that.

For those of you shaking your heads at me and thinking, “Shouldn’t you enjoy your money now instead of waiting until retirement to enjoy it? Life is short!” And I shake my head back.

It’s all about balance, right? I want to be sure that I’m enjoying my life today in this moment (check!) but I also want to be sure that if I get the privilege of living a long and healthy life, that I’m set to retire with decent income. And to do that without having to work until I’m 80 years old (knock on wood), I set aside some of my earnings for retirement.

4. Get a degree to increase earning power.

According to the Census Bureau for the Bureau of Labor Statistics, a bachelor’s degree increases annual earning power by at least $25,000. There are certainly alternative options to a bachelor’s degree, but nonetheless, increasing your level of education can only help you in the long haul. Even with higher education getting exponentially more expensive these days, it’s essential that you get a degree not only to make you more competitive in the job market, but also to earn what you deserve.

5. Start a Roth IRA (and max out your contributions).

Our friend Compound Interest is back and urging you to start a Roth IRA as soon as you can. A Roth IRA is a special kind of individual retirement account (named after Senator William Roth, Jr., one of the legislators behind the Taxpayer Relief Act of 1997) that allows your investments to grow without being taxed. Again, if you start saving now, you will have greater potential to grow more interest on your contributions.

The not-so-secret secret to becoming financially sound is having multiple streams of income and having a diverse investment portfolio. Diversify your portfolio by investing in your employer-sponsored retirement savings program AND in your own Roth IRA. Or if you don’t have the former, just having a Roth IRA is pretty diverse as it is, since you can invest your money in real estate, mutual funds, bonds, money markets, stocks, etc. depending on your risk comfort.

Plus, a huge advantage of having a Roth IRA is that your withdrawals at retirement aren’t taxed! Since you’re setting aside already-taxed money into your Roth, the government can’t touch it a second time. Think about it: say you set aside $5,000 into to your Roth each year starting at age 25, until you retire. Assuming a consistent 7% return, you can withdraw a little over $1 million by retirement age, tax-free. That could pay for a pretty decent standard of living!

So, why wait? Sure, you’ll have to give up a few luxuries today to contribute a few thousands of dollars a year, but Compound Interest will make it worth it down the line.

This sounds too good to be true, and it may be for some. There are certainly requirements and limitations to contributing to a Roth, so be sure to do some research before you jump on it too quickly. Kippler has a great article outlining these requirement/limitations, as well as more of its benefits.

If you’re interested in investing in a traditional IRA, Investopedia does a quick and dirty comparison of the two types.

--------------

There you go - 5 milestones to hit at any age. It’s a good mix of saving, paying down expensive debt, and earning what you deserve. Of course, there are other great financial milestones to consider, like the ones Gen Y Wealth lists. But these 5 really set the foundation for a healthy wallet.

We’d love to hear from you about these milestones! Have you reached and exceeded any of them? Are there any you’re currently working on, or hoping to work on in the future? Tell us in the Comments section below!

RESOURCES:

More financial milestones to consider

Gen Y Wealth

Kiplinger

Yahoo Finance

Articles mentioned in this post

Money Under 30 - How to use a credit card wisely

Money Crashers - How to start and build up your emergency fund in savings

Investopedia - Roth Vs. Traditional IRA: Which is right for you?

Kiplinger - Why you need a Roth IRA

The lesson here is all about the incredible principle of compound interest. The earlier you save, the larger your return will be. At a decent return, even 7 years makes a huge difference. So again, don’t put off for tomorrow what you can do today. Even $50 a month now can mean thousands of dollars down the line.

Personally, retirement benefits are the first thing I look for in a potential employer. Many employers match a percentage of your retirement contribution - which I consider FREE money! If your employer offers this, you should have been taking advantage of this yesterday.

If you don’t have that privilege, consider opening an individual retirement account (IRA) on your own (see number 5). Personally, I have a rollover IRA Fidelity from my first job out of college, but lately I’ve been eyeing Vanguard’s IRAs - a friend of mine loves investing with Vanguard so I will personally be looking into that.

For those of you shaking your heads at me and thinking, “Shouldn’t you enjoy your money now instead of waiting until retirement to enjoy it? Life is short!” And I shake my head back.

It’s all about balance, right? I want to be sure that I’m enjoying my life today in this moment (check!) but I also want to be sure that if I get the privilege of living a long and healthy life, that I’m set to retire with decent income. And to do that without having to work until I’m 80 years old (knock on wood), I set aside some of my earnings for retirement.

4. Get a degree to increase earning power.

According to the Census Bureau for the Bureau of Labor Statistics, a bachelor’s degree increases annual earning power by at least $25,000. There are certainly alternative options to a bachelor’s degree, but nonetheless, increasing your level of education can only help you in the long haul. Even with higher education getting exponentially more expensive these days, it’s essential that you get a degree not only to make you more competitive in the job market, but also to earn what you deserve.

5. Start a Roth IRA (and max out your contributions).

Our friend Compound Interest is back and urging you to start a Roth IRA as soon as you can. A Roth IRA is a special kind of individual retirement account (named after Senator William Roth, Jr., one of the legislators behind the Taxpayer Relief Act of 1997) that allows your investments to grow without being taxed. Again, if you start saving now, you will have greater potential to grow more interest on your contributions.

The not-so-secret secret to becoming financially sound is having multiple streams of income and having a diverse investment portfolio. Diversify your portfolio by investing in your employer-sponsored retirement savings program AND in your own Roth IRA. Or if you don’t have the former, just having a Roth IRA is pretty diverse as it is, since you can invest your money in real estate, mutual funds, bonds, money markets, stocks, etc. depending on your risk comfort.

Plus, a huge advantage of having a Roth IRA is that your withdrawals at retirement aren’t taxed! Since you’re setting aside already-taxed money into your Roth, the government can’t touch it a second time. Think about it: say you set aside $5,000 into to your Roth each year starting at age 25, until you retire. Assuming a consistent 7% return, you can withdraw a little over $1 million by retirement age, tax-free. That could pay for a pretty decent standard of living!

So, why wait? Sure, you’ll have to give up a few luxuries today to contribute a few thousands of dollars a year, but Compound Interest will make it worth it down the line.

This sounds too good to be true, and it may be for some. There are certainly requirements and limitations to contributing to a Roth, so be sure to do some research before you jump on it too quickly. Kippler has a great article outlining these requirement/limitations, as well as more of its benefits.

If you’re interested in investing in a traditional IRA, Investopedia does a quick and dirty comparison of the two types.

--------------

There you go - 5 milestones to hit at any age. It’s a good mix of saving, paying down expensive debt, and earning what you deserve. Of course, there are other great financial milestones to consider, like the ones Gen Y Wealth lists. But these 5 really set the foundation for a healthy wallet.

We’d love to hear from you about these milestones! Have you reached and exceeded any of them? Are there any you’re currently working on, or hoping to work on in the future? Tell us in the Comments section below!

RESOURCES:

More financial milestones to consider

Gen Y Wealth

Kiplinger

Yahoo Finance

Articles mentioned in this post

Money Under 30 - How to use a credit card wisely

Money Crashers - How to start and build up your emergency fund in savings

Investopedia - Roth Vs. Traditional IRA: Which is right for you?

Kiplinger - Why you need a Roth IRA

Copyright © 2015 Jeepney Hub. All Rights Reserved.

RSS Feed

RSS Feed